Choosing between an in-house accountant and outsourced accounting services depends on how much control, flexibility, expertise, and cost efficiency your business needs. While both approaches aim to manage financial operations accurately, they differ significantly in structure, cost, scalability, and long-term impact.

An in-house accountant is an internal employee or team that handles accounting tasks directly within your organization. This model offers immediate access and closer operational involvement but comes with higher fixed costs, staffing responsibilities, and reliance on internal controls.

Outsourced accounting services are provided by third-party accounting firms that manage bookkeeping, reporting, and compliance using standardized processes and modern technology. Outsourcing typically offers broader expertise, predictable pricing, stronger controls, and easier scalability—especially for small and growing businesses.

Understanding the key differences between in-house accountant and outsourcing accounting services helps business owners evaluate which model aligns best with their business size, budget, compliance requirements, and growth goals.

This guide breaks down those differences clearly—covering cost, reporting quality, risk, technology, scalability, and real-world use cases—to help you make an informed decision.

Table of Contents

Key Facts: In-House vs Outsourced Accounting

In-house accounting involves hiring internal employees to manage bookkeeping, reporting, and financial processes within the business, offering direct oversight but higher fixed costs.

Outsourced accounting services are provided by external firms that handle accounting functions using standardized workflows, modern technology, and multi-level review systems.

Cost is a major differentiator: in-house accounting includes salaries, benefits, training, and software, while outsourcing offers predictable monthly pricing with no staffing overhead.

Outsourced accounting provides broader expertise, giving businesses access to a team of professionals instead of relying on a single accountant.

Scalability is easier with outsourcing, allowing businesses to adjust services as transaction volume or complexity changes—without hiring additional staff.

Risk and compliance management are typically stronger with outsourced accounting due to structured controls, documentation, and review processes.

In-house accounting may suit larger organizations with complex daily operations and the resources to maintain full internal controls.

Many growing businesses choose a hybrid approach, combining internal staff with outsourced accounting for reporting, compliance, and oversight.

What Is In-House Accounting?

In-house accounting refers to hiring an internal employee or an internal accounting team that manages your financial operations from within your company. These professionals work directly under your supervision, follow your internal processes, and handle day-to-day financial tasks including bookkeeping, payroll support, reconciliations, and monthly financial reporting.

In this model, all financial activities are performed inside your business, which means you maintain full control, direct oversight, and immediate access to your accounting staff. Because the accountant is part of your team, they typically work on-site or operate as a dedicated remote employee—fully integrated into your business operations, culture, and workflow.

An in-house accountant usually manages:

- Daily bookkeeping and categorization

- Recording income, expenses, receipts, and financial transactions

- Bank & credit card reconciliations

- Payroll data preparation

- Maintaining internal financial processes

- Supporting tax documentation for your CPA

- Preparing internal financial reports for owners or managers

For many small businesses and growing companies, in-house accounting feels familiar and hands-on. However, maintaining an internal accounting function also comes with hiring costs, software expenses, training requirements, and higher operational overhead.

If you want to compare how modern bookkeeping works today, explore how virtual bookkeeping operates here:

What Is Outsourced Accounting?

Outsourced accounting refers to hiring an external, third-party accounting firm to manage your company’s financial operations instead of maintaining a full in-house accounting team. In this model, a specialized accounting provider handles tasks such as bookkeeping, reconciliations, financial reporting, payroll support, tax preparation assistance, and compliance—using secure, cloud-based tools and established workflows.

Unlike an internal employee, outsourced accountants work outside your organization but function as an extension of your business. They deliver the same outcomes as an in-house accountant—clean books, accurate reporting, organized records, and ongoing financial oversight—without the overhead, hiring costs, or training responsibilities associated with maintaining internal staff.

A professional outsourced accounting team typically handles:

- Daily and monthly bookkeeping

- Categorization of income and expenses

- Bank, credit card, and payment-platform reconciliations

- Payroll summaries and employer compliance support

- Sales tax records and documentation

- Month-end closing and financial reporting

- Accounting software setup and automation

- Tax preparation support for your CPA

Most modern outsourced accounting services operate using secure cloud applications like QuickBooks Online, Xero, Dext, and other financial tools—allowing business owners to access real-time financial data anytime.

This approach is especially helpful for small businesses, startups, and growing companies that need accurate financial management but want to avoid the cost and complexity of hiring, training, and supervising an internal accounting department.

To understand how outsourced bookkeeping works in detail, explore our comprehensive guide:

Core Differences Between In-House vs Outsourced Accounting

Understanding the core differences between in-house and outsourced accounting helps business owners decide which model offers the right balance of control, cost efficiency, expertise, and long-term scalability. While both approaches aim to maintain accurate financial records, the way each model operates—and the level of value it delivers—can be very different.

Here are the key differences at a glance:

1. Control & Visibility

- In-house: Full control, real-time visibility, direct oversight of daily accounting tasks.

- Outsourced: Structured workflows and scheduled reporting; visibility through dashboards and monthly/weekly updates.

2. Cost Structure

- In-house: Higher costs due to salaries, benefits, training, turnover, office space, and accounting software.

- Outsourced: Predictable monthly fees, no hiring or training cost, and no overhead expenses.

3. Expertise & Skill Level

- In-house: Expertise depends on the individual employee(s); may require ongoing training.

- Outsourced: Access to a full team of trained accountants with broader industry experience and specialized skills.

4. Scalability

- In-house: Limited; growing businesses may outgrow a single accountant or small team.

- Outsourced: Easily scalable; firms can increase capacity during peak seasons or business growth phases.

5. Workflow & Efficiency

- In-house: Manual processes handled internally; speed and accuracy depend on the team’s workload and experience.

- Outsourced: Streamlined workflows using cloud-based tools, automation, and established processes to reduce errors.

6. Software & Technology

- In-house: Requires the business to purchase and maintain accounting software and tools.

- Outsourced: Technology is included; firms use advanced software, automation, and integrated systems for accuracy and faster turnaround.

7. Compliance & Risk Management

- In-house: Internal controls depend on your staff; higher risk of errors and compliance gaps if the team is small.

- Outsourced: Built-in compliance, multi-level review systems, and lower risk of financial reporting errors or missed deadlines.

8. Business Focus

- In-house: Owners often spend time managing accounting tasks or supervising staff.

- Outsourced: Frees up owners to focus on core operations, growth, and decision-making.

9. Reporting & Financial Insights

- In-house: Reporting quality varies depending on the accountant’s skill level and workload.

- Outsourced: Consistent, accurate, and timely financial reports using standardized processes.

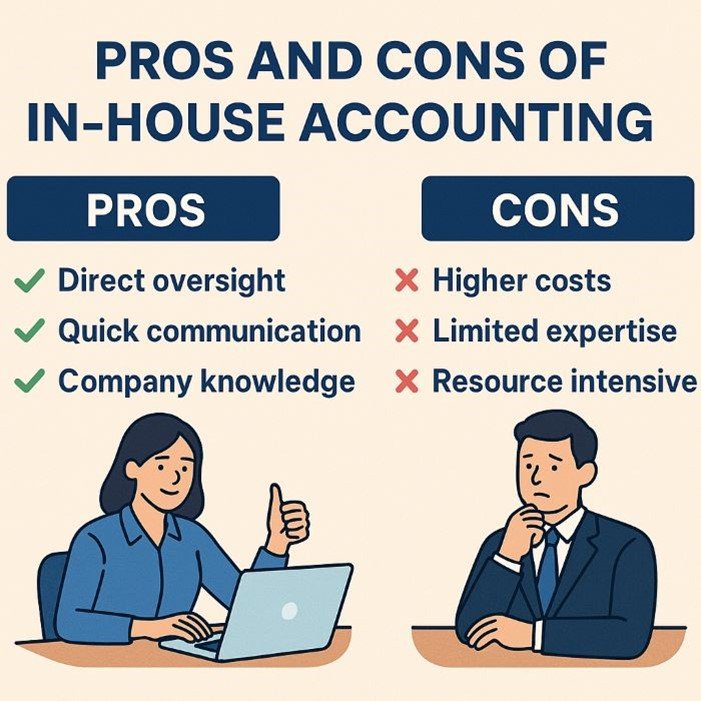

Pros and Cons of In-House Accounting

In-house accounting gives business owners direct control over their financial operations, but it also comes with costs, staffing responsibilities, and limitations. Understanding the strengths and weaknesses of this model helps determine whether maintaining an internal accounting function is practical for your business.

Advantages of In-House Accounting

1. Full Control and Immediate Access

Your accounting staff is part of your internal team, giving you real-time visibility into transactions, reports, and financial processes. You can request updates, clarifications, and custom reports anytime without waiting for an external provider’s schedule.

2. Deeper Knowledge of Your Business

Internal accountants understand your operations, customers, workflows, and industry-specific financial patterns. This familiarity helps them identify issues faster and tailor financial processes to your exact business needs.

3. Direct Communication and Collaboration

In-house accountants work closely with managers, operations, and sales teams. This improves coordination, reduces information gaps, and enables quicker decision-making based on up-to-date financial data.

4. Immediate Support During Urgent Situations

If something requires urgent attention—such as vendor disputes, payroll adjustments, or reporting questions—internal staff can respond instantly.

Disadvantages of In-House Accounting

1. Higher Costs and Employee Overhead

Maintaining an in-house accountant requires paying:

- Salary

- Payroll taxes

- Employee benefits

- Training

- Software subscriptions

- Office equipment

- HR and onboarding costs

For many small and mid-sized businesses, these costs exceed the benefits of having a full-time internal accountant.

2. Limited Expertise

A single employee or small internal team may not have complete expertise in:

- Advanced accounting

- Tax strategy

- Multi-state compliance

- Payroll regulations

- Sales tax rules

- IRS documentation requirements

This often leads to knowledge gaps and risk exposure.

3. Risk of Turnover

If your only accountant leaves:

- You lose institutional financial knowledge

- Books may fall behind

- Re-hiring and re-training take time

- Compliance deadlines can be missed

This creates instability in financial operations.

4. Potential for Errors or Fraud

Small internal teams often lack segregation of duties.

This increases risk of:

- Misreporting

- Incorrect categorization

- Missed reconciliations

- Internal fraud opportunities

Lack of review layers can affect accuracy and compliance.

5. Scalability Challenges

As your business grows, a single accountant may not keep up with:

- Higher transaction volume

- New revenue streams

- Payroll expansion

- Multi-entity reporting

Scaling an internal team is expensive and time-consuming.

Pros and Cons of Outsourced Accounting Services

Outsourced accounting allows businesses to delegate their financial management to a specialized external firm. This approach reduces operational burden, improves accuracy, and provides access to expert-level accounting support—without the costs and complexities of hiring and managing internal staff. However, like any model, it has both benefits and limitations you should understand before deciding.

Advantages of Outsourcing Accounting

1. Cost Savings and Predictable Pricing

Outsourcing eliminates the largest internal expenses such as:

- Salaries

- Employee benefits

- Training

- Accounting software

- Office space or equipment

Most outsourced accounting firms offer flat-rate or fixed monthly pricing, making budgeting easier for small and mid-sized businesses.

2. Access to Specialized Expertise

Instead of relying on a single general accountant, outsourcing provides access to a full team of professionals skilled in:

- Bookkeeping

- Financial reporting

- Payroll support

- Sales tax

- Compliance

- Multi-state accounting

- Industry-specific workflows

This ensures greater accuracy, stronger internal controls, and better financial insights.

3. Scalability and Flexibility

As your business grows, outsourced teams can easily scale up services—handling increased transactions, new revenue streams, or expanded reporting needs without requiring you to hire additional staff.

Similarly, if operations slow down, you can scale services back without affecting your internal workforce.

4. Better Use of Technology and Automation

Reputable outsourced accounting firms use:

- Advanced cloud-based accounting systems

- Automation tools

- Reconciliation software

- AI-powered categorization

- Real-time dashboards

This improves speed, accuracy, and reporting quality while reducing manual errors.

5. Reduced Risk and Stronger Compliance

Because outsourced firms follow standardized processes and multi-step review systems, they reduce risks such as:

- Incorrect categorization

- Missed reconciliations

- Compliance lapses

- Payroll and sales tax errors

- Late filings

Specialized accounting teams stay current on IRS rules, state requirements, and GAAP standards.

6. Frees Up Time for Business Owners

With financial management handled externally, owners can focus more on:

- Growth

- Operations

- Customer service

- Strategic decisions

Instead of supervising accounting staff or troubleshooting errors.

Disadvantages of Outsourcing Accounting

1. Less Direct Control

You do not have accountants physically present in your office.

Communication is structured, and reporting occurs on scheduled timelines—although real-time dashboards can minimize this gap.

2. Communication Delays (Sometimes)

If your provider has slower response times or limited availability, small delays can occur.

However, reputable firms provide dedicated support channels and predictable turnaround times.

3. Dependency on a Third-Party Provider

Your business becomes reliant on an external partner for financial operations.

This makes choosing a reliable, secure, and transparent accounting firm extremely important.

4. Security & Privacy Concerns (When Using Low-Quality Providers)

Poorly-managed outsourcing companies may lack proper:

- Data security

- Encryption

- Access controls

- Compliance policies

Professional U.S.-based accounting providers avoid these issues by using secure cloud platforms and standardized internal controls.

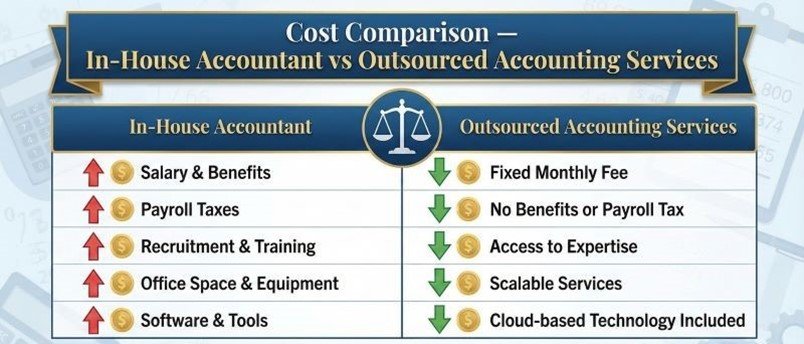

Cost Comparison — In-House Accountant vs Outsourced Accounting Services

Cost is often the deciding factor when businesses compare in-house accounting with outsourced accounting services. While an internal accountant may seem straightforward at first, the true cost goes far beyond salary. Outsourced accounting, on the other hand, offers a more predictable and scalable pricing model.

Below is a clear breakdown to help business owners understand the real financial impact of both options.

In-House Accounting Costs

Hiring an in-house accountant involves fixed and ongoing expenses, including:

- Base salary (full-time or part-time)

- Payroll taxes and employee benefits

- Paid time off, sick leave, and holidays

- Training and continuing education

- Accounting software licenses

- Office space, equipment, and IT support

- Recruitment, onboarding, and HR management

- Cost of turnover and re-hiring

Even for small businesses, these costs add up quickly—especially when a single accountant cannot handle growing transaction volume or complex compliance needs.

Outsourced Accounting Costs

Outsourced accounting services typically operate on monthly, flat-rate, or tiered pricing, based on:

- Transaction volume

- Business size and complexity

- Reporting requirements

- Payroll or sales tax support

- Software integrations

With outsourcing, businesses avoid:

- Salaries and benefits

- Hiring and training expenses

- Software purchasing and maintenance

- Office and infrastructure costs

You pay only for the level of service you need—making outsourced accounting more flexible and cost-efficient for most small and mid-sized businesses.

Side-by-Side Cost Comparison

| Cost Area | In-House Accountant | Outsourced Accounting |

|---|---|---|

| Salary & Benefits | High, fixed | Not required |

| Software & Tools | Business pays | Included |

| Training | Ongoing | Included |

| Scalability | Expensive | Built-in |

| Turnover Risk | High impact | Minimal |

| Monthly Predictability | Low | High |

| Long-Term Cost Control | Difficult | Easier |

Which Option Is More Cost-Effective?

- In-house accounting may make sense for large businesses with complex, daily accounting needs and sufficient budget.

- Outsourced accounting is usually more cost-effective for startups, small businesses, and growing companies that want expert support without long-term overhead.

Cost alone should not be the only factor—but understanding the full financial picture helps business owners make a smarter, more sustainable decision.

Differences in Reporting, Accuracy & Financial Management

The way financial data is recorded, reviewed, and reported plays a critical role in business decision-making. While both in-house and outsourced accounting aim to keep books accurate, the quality, consistency, and reliability of financial management can differ significantly between the two models.

Financial Reporting Quality

In-house accounting:

Reporting quality depends heavily on the experience and workload of the internal accountant. If one person handles everything, reports may be delayed, simplified, or lack deeper analysis—especially during busy periods.

Outsourced accounting:

Reports are prepared using standardized processes and reviewed by multiple professionals. This usually results in more consistent, accurate, and timely financial statements, including profit & loss, balance sheet, and cash flow reports.

Accuracy & Error Reduction

In-house:

Manual processes, limited review layers, and workload pressure increase the risk of:

- Misclassified transactions

- Missed reconciliations

- Incomplete records

- Inconsistent reporting

Outsourced:

Outsourced accounting firms use multi-step review systems, automation, and reconciliation checks, significantly reducing errors and improving data accuracy.

Financial Management & Oversight

In-house:

Financial management is often reactive. Internal teams focus on keeping up with daily tasks rather than providing strategic insights or proactive monitoring.

Outsourced:

Outsourced providers follow structured monthly workflows and monitoring systems. Business owners receive organized, review-ready financial data that supports forecasting, planning, and informed decision-making.

Consistency & Timeliness

In-house:

Reports may be delayed due to vacations, sick days, or competing priorities.

Outsourced:

Reporting timelines are contract-based and predictable, ensuring on-time delivery of financial reports every month.

Decision-Making Impact

Clean, accurate, and timely financial data allows business owners to:

- Track profitability

- Control cash flow

- Identify unnecessary expenses

- Plan for growth

- Prepare confidently for tax season

In most cases, outsourced accounting provides higher consistency and reliability, while in-house accounting offers immediacy but depends strongly on individual performance.

Automation, Accounting Software & Technology Differences

Technology plays a major role in how efficiently accounting tasks are handled. One of the biggest differences between in-house and outsourced accounting lies in how automation, accounting software, and financial tools are used to improve accuracy, speed, and visibility.

Technology in In-House Accounting

With an in-house accounting setup, businesses are responsible for selecting, purchasing, maintaining, and updating their own accounting software. The level of automation largely depends on budget, technical expertise, and internal adoption.

Common challenges include:

- Limited use of automation due to cost constraints

- Manual data entry and reconciliations

- Delayed software updates

- Dependence on a single system or user

- Higher risk of errors when processes are manual

Many small businesses rely on basic accounting software but underutilize advanced features such as automation rules, integrations, or real-time dashboards—mainly due to time and training limitations.

Technology in Outsourced Accounting

Outsourced accounting firms are built around modern, cloud-based accounting technology. These providers invest heavily in tools that improve efficiency, accuracy, and reporting quality.

Outsourced accounting typically includes:

- Cloud accounting software (e.g., QuickBooks Online, Xero)

- Automated transaction imports and categorization

- Bank and credit card integrations

- Receipt capture and document management tools

- Payroll and payment system integrations

- Real-time financial dashboards

- Automated reconciliation workflows

Because these tools are included as part of the service, businesses benefit from enterprise-level technology without additional cost or setup effort.

Automation & Efficiency Comparison

In-house:

Automation is limited by internal resources, training, and budget. Manual processes often increase workload and error risk.

Outsourced:

Automation is a core part of service delivery, reducing manual work, improving accuracy, and speeding up month-end close.

Impact on Business Operations

Better technology leads to:

- Faster reporting

- Cleaner data

- Improved cash flow visibility

- Easier collaboration with CPAs and tax professionals

- Stronger compliance readiness

For most small and growing businesses, outsourced accounting provides more advanced technology and automation than an internal setup can realistically support.

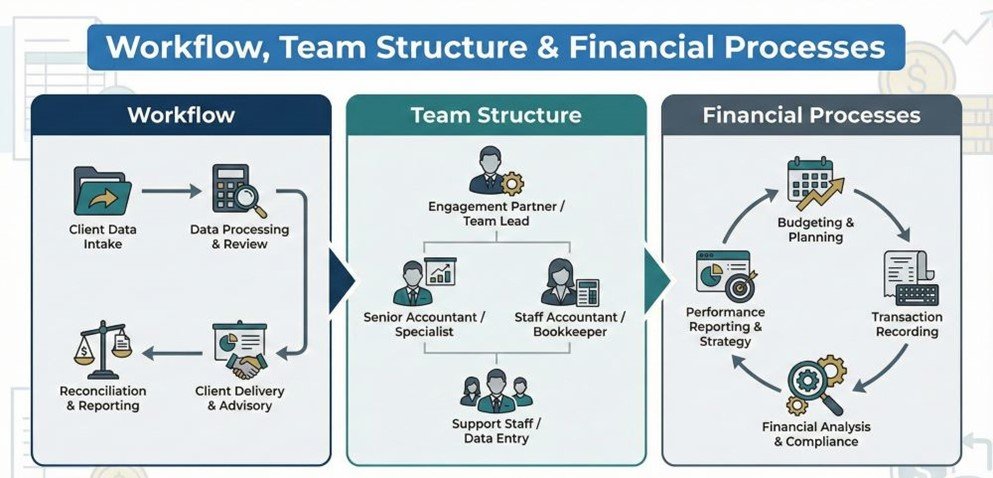

Workflow, Team Structure & Financial Processes

The structure of your accounting team and the way financial processes are managed can significantly affect accuracy, efficiency, and long-term stability. In-house and outsourced accounting follow very different workflows, which directly impacts how smoothly financial operations run.

Team Structure

In-house accounting:

Typically relies on one accountant or a small internal team. Responsibilities are centralized, which can be efficient initially but risky if workload increases or key staff become unavailable.

Outsourced accounting:

Uses a team-based model, where multiple professionals handle different aspects of your accounting. This ensures continuity, built-in review processes, and coverage even when someone is unavailable.

Daily & Monthly Financial Processes

In-house:

Financial processes depend on internal capacity and prioritization. Month-end close, reconciliations, and reporting may be delayed during busy periods or staffing gaps.

Outsourced:

Outsourced firms follow standardized, repeatable workflows. Daily tasks, month-end close, reconciliations, and reporting are completed on fixed schedules using documented processes.

Process Consistency & Documentation

In-house:

Processes are often informal or undocumented, especially in small teams. This can lead to inconsistency and errors when responsibilities shift.

Outsourced:

Financial processes are clearly documented, monitored, and reviewed. This consistency improves accuracy, audit readiness, and compliance.

Reliability & Continuity

In-house:

Vacations, sick leave, or employee turnover can interrupt financial operations and reporting timelines.

Outsourced:

Work continues uninterrupted because responsibilities are distributed across a team with backup support.

Operational Impact for Business Owners

A structured workflow reduces stress for business owners by ensuring:

- Predictable reporting timelines

- Clean and organized financial records

- Reduced dependency on one individual

- Better visibility into financial performance

For most businesses, outsourced accounting provides more stable and reliable financial processes, while in-house accounting offers closer day-to-day involvement but with higher operational risk.

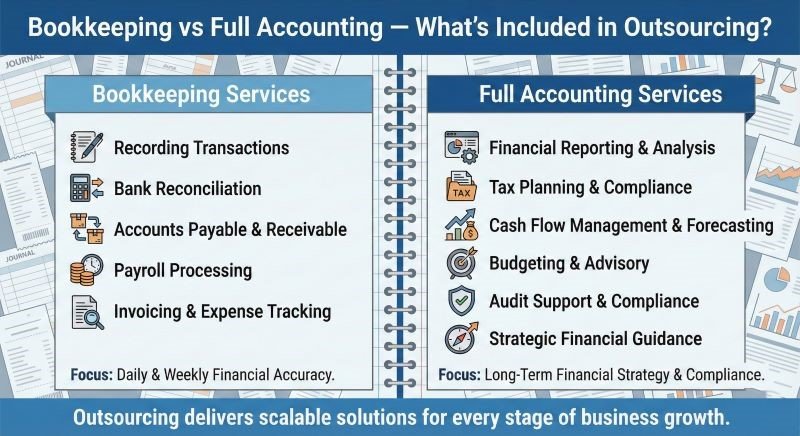

Bookkeeping vs Full Accounting — What’s Included in Outsourcing?

Many business owners assume that bookkeeping and accounting are the same—but they serve different roles. Understanding this difference is essential when comparing in-house accounting with outsourced accounting services, especially since most outsourcing providers cover both.

What Bookkeeping Covers

Bookkeeping focuses on recording and organizing financial transactions. It is the foundation of accurate financial reporting.

Typical bookkeeping tasks include:

- Recording income and expenses

- Categorizing transactions

- Managing receipts and invoices

- Bank and credit card reconciliations

- Maintaining general ledgers

- Tracking accounts payable and receivable

Bookkeeping ensures your financial data is clean, up to date, and ready for review—but it does not provide strategic insights on its own.

What Full Accounting Includes

Accounting builds on bookkeeping data and turns it into meaningful financial insight. It focuses on analysis, reporting, and compliance.

Full accounting typically includes:

- Reviewing and validating bookkeeping entries

- Preparing financial statements (P&L, balance sheet, cash flow)

- Monitoring financial performance

- Supporting tax preparation and compliance

- Advising on financial structure and controls

- Identifying risks, trends, and inefficiencies

How Outsourced Accounting Combines Both

Most outsourced accounting services include both bookkeeping and accounting as part of a single, integrated service.

This means businesses receive:

- Daily or monthly bookkeeping

- Ongoing review by accounting professionals

- Structured month-end close

- Accurate financial reports

- Compliance-ready records

In contrast, in-house setups often rely on a single accountant handling both roles—without the layered review or specialized oversight that outsourcing provides.

Why This Matters for Business Owners

When bookkeeping and accounting are handled together:

- Errors are caught earlier

- Reports are more reliable

- Tax season is smoother

- Financial decisions are based on accurate data

Outsourced accounting offers a more complete financial solution, especially for businesses that need both day-to-day bookkeeping and higher-level accounting support without hiring multiple internal staff members.

Risk, Compliance & Internal Controls

Risk management and compliance are often overlooked when businesses compare in-house and outsourced accounting. However, weak controls or missed compliance requirements can lead to financial errors, penalties, audits, and long-term operational risk.

The way each accounting model handles controls and oversight makes a significant difference.

Risk Exposure in In-House Accounting

In-house accounting teams—especially small ones—often face higher risk due to limited checks and balances.

Common risk areas include:

- Lack of segregation of duties (one person handles multiple tasks)

- Limited internal review of financial entries

- Greater dependency on a single employee

- Higher chance of unnoticed errors or misclassifications

- Increased fraud risk in small teams

When one accountant records transactions, reconciles accounts, and prepares reports without independent review, mistakes can go undetected for long periods.

Risk Management in Outsourced Accounting

Outsourced accounting firms are structured to reduce risk through layered controls and standardized procedures.

These typically include:

- Separation of bookkeeping and review functions

- Multi-level quality checks

- Documented workflows and approvals

- Automated reconciliation checks

- Secure access controls and permissions

Because work is distributed across a team, errors are more likely to be caught early—before they impact reporting or compliance.

Compliance Responsibilities

Accounting compliance goes beyond basic bookkeeping and includes:

- IRS record-keeping requirements

- Payroll tax documentation

- Sales tax tracking

- State and federal reporting deadlines

- Audit readiness

In-house accounting:

Compliance depends on the knowledge and experience of your internal staff. If regulations change or deadlines are missed, the business bears full responsibility.

Outsourced accounting:

Professional firms stay updated on regulatory changes and follow structured compliance workflows, reducing the risk of missed filings or incorrect reporting.

Internal Controls & Audit Readiness

Strong internal controls ensure financial accuracy and protect business assets.

In-house:

Controls may be informal or undocumented, making audits more difficult and increasing exposure to errors.

Outsourced:

Standardized documentation, consistent reporting, and organized records improve audit readiness and financial transparency.

Why This Matters for Business Owners

Poor internal controls and compliance gaps can result in:

- IRS notices or penalties

- Cash flow issues

- Inaccurate financial decisions

- Loss of trust from partners or investors

For most small and growing businesses, outsourced accounting provides stronger risk management and compliance support, while in-house accounting requires careful oversight and additional internal controls to achieve the same level of protection.

Scalability, Growth & Specialized Expertise

As a business grows, its accounting needs become more complex. Transaction volume increases, reporting requirements expand, and compliance responsibilities grow. One of the key differences between in-house and outsourced accounting is how well each model adapts to change and provides the expertise needed at different growth stages.

Scalability Challenges with In-House Accounting

In-house accounting teams are often designed for a specific workload. As the business grows, challenges can include:

- Increased transaction volume that overwhelms existing staff

- Need to hire additional accountants or support roles

- Rising payroll and benefit costs

- Delays in reporting during growth periods

- Difficulty keeping up with new compliance requirements

Scaling an internal accounting function usually requires additional hiring, training, and infrastructure, which can be slow and expensive.

Scalability Advantages of Outsourced Accounting

Outsourced accounting is built to scale. Services can be adjusted as your business changes, without restructuring your internal team.

Outsourcing allows businesses to:

- Add or reduce services as needed

- Handle seasonal or rapid growth smoothly

- Support new locations, entities, or revenue streams

- Increase reporting depth without hiring new staff

This flexibility makes outsourced accounting ideal for startups, growing companies, and businesses planning expansion.

Access to Specialized Expertise

In-house accounting:

Expertise depends on the background of one accountant or a small team. Specialized knowledge—such as multi-state accounting, payroll compliance, or advanced reporting—may be limited.

Outsourced accounting:

Provides access to a team with diverse skills and experience across industries, business sizes, and compliance scenarios. This includes expertise in:

- Financial reporting

- Payroll and sales tax

- Industry-specific accounting

- Regulatory compliance

- Process optimization

This depth of expertise reduces risk and improves financial decision-making.

Long-Term Business Impact

As businesses grow, financial accuracy and insight become more important—not less. Reliable accounting support helps owners:

- Plan expansion confidently

- Control costs during growth

- Maintain compliance

- Present accurate financials to lenders or investors

For most growing businesses, outsourced accounting offers greater scalability and access to expertise, while in-house accounting may require continuous investment to keep up.

When In-House Accounting Makes Sense

Although outsourced accounting is the better option for many small and growing businesses, there are situations where maintaining an in-house accountant or accounting team can make sense. The right choice depends on your company’s size, operational complexity, and internal resources.

Below are scenarios where in-house accounting may be a suitable fit.

You Have a Large, Established Operation

Businesses with high daily transaction volume, multiple departments, and complex internal workflows may benefit from having accountants physically embedded within the organization. In such cases, real-time, on-site coordination can support operational efficiency.

You Need Constant, Real-Time Internal Interaction

If your accounting team needs to work closely with operations, inventory, production, or finance leadership throughout the day, in-house accounting can offer faster internal collaboration—especially in highly operational environments.

You Can Support a Full Accounting Team

In-house accounting works best when businesses can afford:

- Multiple accounting staff

- Proper segregation of duties

- Ongoing training

- Accounting software and systems

- Internal controls and review processes

A single in-house accountant handling everything often creates risk rather than efficiency.

You Have Strong Internal Controls in Place

If your business already has well-defined financial policies, documented processes, and internal review systems, an in-house accounting team can operate effectively with lower risk of errors or compliance issues.

You Require Industry-Specific, On-Site Expertise

Certain industries or business models may require accountants who are deeply embedded in day-to-day operations or proprietary systems. In these cases, in-house accounting can provide tailored support that external firms may not easily replicate.

Important Consideration for Business Owners

In-house accounting is rarely cost-effective for small or mid-sized businesses unless supported by adequate staffing and controls. Without those, risks related to errors, turnover, and compliance often outweigh the benefits.

When Outsourced Accounting Is the Better Option

For many small and mid-sized businesses, outsourced accounting is the more practical, cost-effective, and scalable choice. It allows business owners to access professional accounting support without the burden of hiring, managing, and maintaining an internal team.

Below are common situations where outsourcing accounting services makes the most sense.

You Want to Reduce Costs Without Sacrificing Quality

Outsourced accounting eliminates fixed costs such as salaries, benefits, training, and software. Instead, businesses pay a predictable monthly fee based on actual needs—making it easier to control expenses while still receiving high-quality accounting support.

Your Business Is Growing or Changing Quickly

When transaction volume increases, new revenue streams are added, or operations expand, outsourced accounting can scale immediately—without hiring delays or restructuring internal teams.

This flexibility is especially valuable for startups, seasonal businesses, and companies planning expansion.

You Need Broader Expertise Than One Accountant Can Provide

Outsourcing gives access to a team of professionals with experience across:

- Bookkeeping and accounting

- Payroll and sales tax

- Financial reporting

- Compliance and documentation

- Industry-specific accounting needs

This depth of expertise reduces risk and improves financial accuracy.

You Want Reliable Reporting Without Internal Disruptions

Outsourced accounting ensures continuity even when staff changes occur. Reporting timelines remain consistent, and financial processes continue uninterrupted—regardless of vacations, sick days, or turnover.

You Want Stronger Controls and Compliance Support

Professional accounting firms use standardized workflows, review systems, and secure technology to reduce errors and maintain compliance with IRS and state requirements.

This lowers the risk of missed deadlines, inaccurate records, or compliance-related issues.

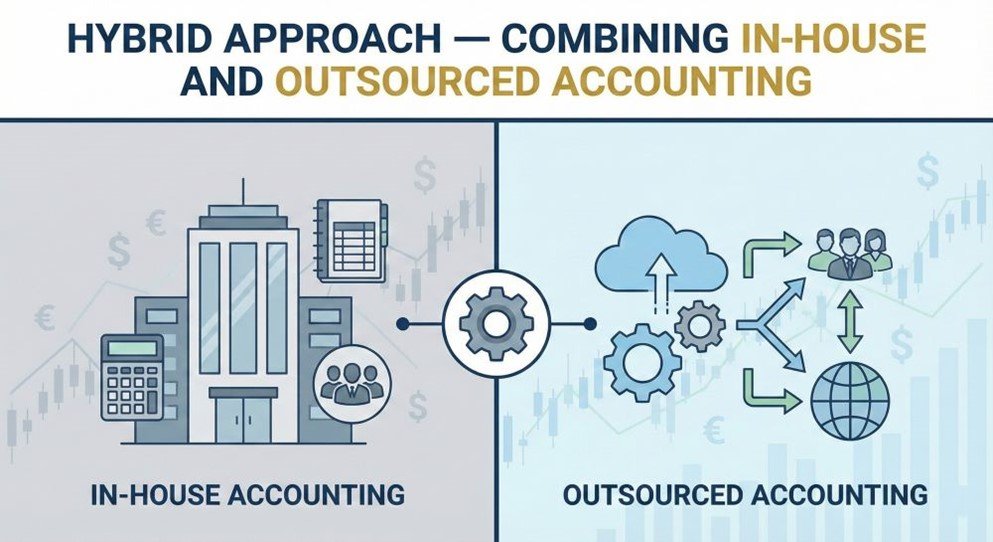

Hybrid Approach — Combining In-House and Outsourced Accounting

Some businesses don’t fit neatly into a fully in-house or fully outsourced accounting model. In these cases, a hybrid accounting approach—combining internal staff with outsourced accounting support—can offer the best of both worlds.

This model allows businesses to keep certain accounting functions internal while outsourcing specialized, time-consuming, or compliance-heavy tasks to external experts.

How a Hybrid Accounting Model Works

In a hybrid setup:

In-house staff handle day-to-day operational tasks such as:

- Basic bookkeeping

- Invoice processing

- Internal coordination with departments

- Routine financial data entry

Outsourced accounting partners manage higher-level responsibilities like:

- Monthly reconciliations and reviews

- Financial reporting

- Compliance oversight

- Payroll and sales tax support

- Process optimization

- CPA and tax-preparation coordination

This division of responsibility improves efficiency without overloading internal teams.

Benefits of a Hybrid Approach

A well-structured hybrid model can offer several advantages:

- Maintains internal visibility and operational control

- Reduces workload on in-house staff

- Provides access to specialized accounting expertise

- Improves accuracy through external review

- Enhances compliance and audit readiness

- More cost-effective than building a full internal accounting department

Challenges to Consider

Hybrid accounting only works when roles are clearly defined. Without proper coordination, businesses may face:

- Duplication of work

- Communication gaps

- Accountability issues

To avoid these problems, businesses should establish clear workflows, reporting responsibilities, and review processes between internal staff and outsourced partners.

When a Hybrid Model Makes Sense

A hybrid approach is often ideal when:

- A business has internal staff but lacks advanced accounting expertise

- Transaction volume is growing but not enough to justify a full team

- Compliance requirements are increasing

- Owners want stronger controls without losing internal visibility

When implemented correctly, a hybrid model provides flexibility, accuracy, and scalability—without the cost and complexity of a fully in-house accounting department.

Decision Matrix — How to Choose the Right Option

Choosing between in-house accounting and outsourced accounting services depends on your business size, budget, complexity, and long-term goals. Instead of guessing, use the decision matrix below to evaluate which option aligns best with your needs.

In-House vs Outsourced Accounting: Decision Matrix

| Business Factor | In-House Accounting | Outsourced Accounting |

|---|---|---|

| Business Size | Medium to large organizations | Startups, small & growing businesses |

| Budget Flexibility | Requires higher fixed costs | Predictable monthly pricing |

| Transaction Volume | Very high, daily operations | Low to high, scalable |

| Need for Specialized Expertise | Limited to hired staff | Access to full expert team |

| Compliance Complexity | Requires internal expertise | Built-in compliance support |

| Technology & Automation | Business must invest | Included with service |

| Risk & Internal Controls | Depends on internal setup | Strong multi-level controls |

| Scalability | Costly and slow | Fast and flexible |

| Owner Involvement | High (management required) | Low (handled externally) |

| Focus on Core Business | Reduced | Increased |

Quick Self-Assessment Questions

If you answer “yes” to most of the following, outsourced accounting may be the better fit:

- Do you want to reduce overhead and fixed payroll costs?

- Do you need reliable financial reporting without managing staff?

- Is compliance becoming more complex as your business grows?

- Do you want access to expert support without hiring multiple employees?

- Would you rather focus on running your business than supervising accounting tasks?

If you answer “yes” to these instead, in-house accounting may make sense:

- Do you have the budget for a full accounting team?

- Do you need constant, on-site financial coordination?

- Are strong internal controls already in place?

- Does your business require daily internal accounting involvement?

Making the Right Choice

There is no one-size-fits-all answer. The right accounting model depends on how much control, flexibility, expertise, and cost efficiency your business requires.

Many businesses start with outsourced accounting, move to a hybrid model as they grow, and only build a full in-house team when scale and complexity justify it.

Frequently Asked Questions

What is the difference between outsourced accounting and in-house accounting?

The main difference lies in who manages the accounting and how it is structured.

In-house accounting is handled by an internal employee or team working directly within your business. Outsourced accounting is managed by a third-party firm that provides bookkeeping, reporting, and compliance support using standardized systems and specialized expertise.

Outsourced accounting is typically more scalable and cost-efficient, while in-house accounting offers closer day-to-day involvement.

What is the difference between in-house and outsourcing?

In-house means hiring employees internally to perform accounting tasks. Outsourcing means delegating those tasks to an external accounting service provider.

In-house accounting involves fixed costs such as salaries, benefits, and software. Outsourcing converts these into a predictable service cost and provides access to a full accounting team rather than relying on one individual.

What are the benefits of in-house accounting?

In-house accounting offers:

- Direct control and oversight

- Immediate access to accounting staff

- Closer integration with internal operations

- Familiarity with company processes and culture

However, these benefits usually require sufficient staffing, internal controls, and budget to be effective.

What does an in-house accountant do?

An in-house accountant typically manages:

- Daily bookkeeping and transaction recording

- Bank and credit card reconciliations

- Payroll data preparation

- Internal financial reporting

- Maintaining accounting records and processes

- Supporting tax documentation for external CPAs

Responsibilities vary based on business size and complexity.

Should I hire an in-house accountant?

Hiring an in-house accountant may make sense if your business has:

- High daily transaction volume

- The budget for salaries, benefits, and software

- Strong internal controls and review processes

- Ongoing need for on-site financial coordination

For many small businesses, outsourced accounting is often a more practical starting point.

Is it better to outsource accounting?

For most small and growing businesses, yes. Outsourcing accounting provides access to experienced professionals, better controls, and modern technology—without the overhead of hiring and managing an internal team.

Outsourcing is especially beneficial when cost control, scalability, and compliance support are priorities.

Is outsourcing cheaper than in-house accounting?

In most cases, yes. Outsourced accounting eliminates costs such as:

- Salaries and employee benefits

- Training and onboarding

- Accounting software licenses

- Office space and equipment

Instead, businesses pay a predictable monthly fee based on their needs.

Is it cheaper to outsource accounting?

Outsourcing is generally more cost-effective for small and mid-sized businesses. While costs vary by service level, outsourcing often delivers better value by combining bookkeeping, accounting, reporting, and compliance support under one service model.

How much does outsourced bookkeeping cost?

Outsourced bookkeeping costs depend on transaction volume, service scope, and business complexity. Most small businesses pay a monthly fee, which is typically lower than the total cost of hiring a full-time bookkeeper or accountant.

Are bookkeepers cheaper than accountants?

Yes. Bookkeepers generally handle transactional tasks and are less expensive than accountants, who provide analysis, reporting, and compliance oversight.

Many outsourced accounting services combine both bookkeeping and accounting, offering better overall value than hiring separate roles.

Can a business use both in-house and outsourced accounting together?

Yes. Many businesses use a hybrid model, where internal staff manage daily tasks and outsourced professionals handle reporting, compliance, and review. This approach offers flexibility while maintaining internal visibility.

What is the difference between in-house internal audit and outsourcing?

In-house internal audits are performed by employees who understand internal operations closely. Outsourced audits are conducted by independent professionals who provide objective reviews and specialized compliance expertise.

Outsourced audits often reduce bias and strengthen compliance, while in-house audits offer operational familiarity.

Final Thoughts

Choosing between an in-house accountant and outsourced accounting services is not about which option is universally better—it’s about what fits your business at its current stage.

In-house accounting offers direct oversight and internal integration, but it comes with higher fixed costs, staffing challenges, and greater responsibility for controls and compliance. It works best for larger organizations with the resources to support a full accounting function.

Outsourced accounting, on the other hand, provides flexibility, access to specialized expertise, modern technology, and structured processes without the burden of managing an internal team. For many small and growing businesses, outsourcing delivers more reliable financial management at a predictable cost.

Some businesses benefit from a hybrid approach—keeping basic tasks in-house while relying on outsourced professionals for reporting, compliance, and oversight. This model allows companies to maintain internal visibility while reducing risk and operational strain.

Ultimately, the right decision depends on your business size, budget, complexity, and growth goals. Understanding the key differences between in-house accounting and outsourcing accounting services helps business owners make informed, strategic financial decisions that support long-term stability and growth.